U.S. Economy Rebounded in Second Quarter

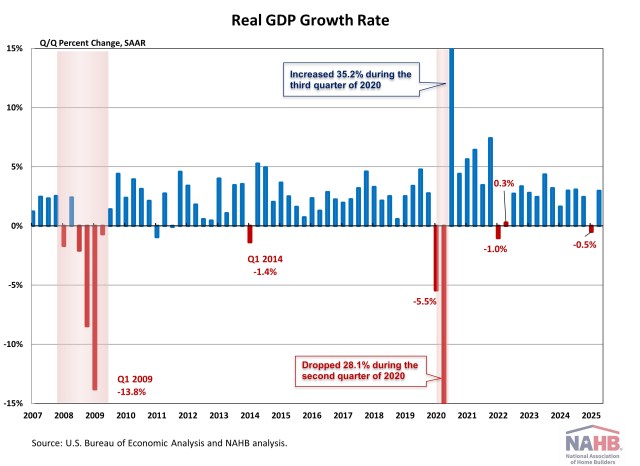

Web Master2025-08-13T11:16:12-05:00Real GDP growth rebounded in the second quarter, driven by a turnaround in the trade balance and stronger consumer spending. According to the “advance” estimate released by the Bureau of Economic Analysis (BEA), real gross domestic product (GDP) expanded at an annual rate of 3.0% in the second quarter of 2025, following a 0.5% contraction in the first quarter. The latest data from the GDP report suggests that inflationary pressures are easing. The GDP price index rose 2.0% for the second quarter, down from a 3.8% increase in the first quarter of 2025. The Personal Consumption Expenditures Price (PCE) Index, which measures inflation (or deflation) across various consumer expenses and reflects changes in consumer behavior, rose 2.1% in the second quarter. This is down from a 3.7% increase in the first quarter of 2025. This quarter’s increase in real GDP primarily reflected a decrease in imports, which are a subtraction in the calculation of GDP, and increases in consumer spending. Consumer spending, the backbone of the U.S. economy, rose at an annual rate of 1.4% in the second quarter, up from 0.5% in the first quarter but well below the 2.8% pace recorded a year earlier. Both goods and services contributed to the gain, with goods spending rising at a 2.2% annual rate and spending on services increasing at a 1.1% annual rate. A steep drop in imports also provided a significant boost to GDP, as imports are subtracted in GDP calculations. Imports fell 30.3% in the second quarter, a sharp reversal from the 37.9% surge in the first quarter. Nonresidential fixed investment increased 1.9% in the second quarter. The increases in equipment (+4.8%) and intellectual property products (+6.4%) offset the decrease in structures (-10.3%). Meanwhile, residential fixed investment (RFI) declined 4.6% in the second quarter, following a 1.3% decline in the previous quarter. Within the residential category, single-family structures fell 12.6% at an annual rate, multifamily structures declined 1.3%, and improvements rose 4.2%. For the common BEA terms and definitions, please access bea.gov/Help/Glossary. Discover more from Eye On Housing Subscribe to get the latest posts sent to your email.