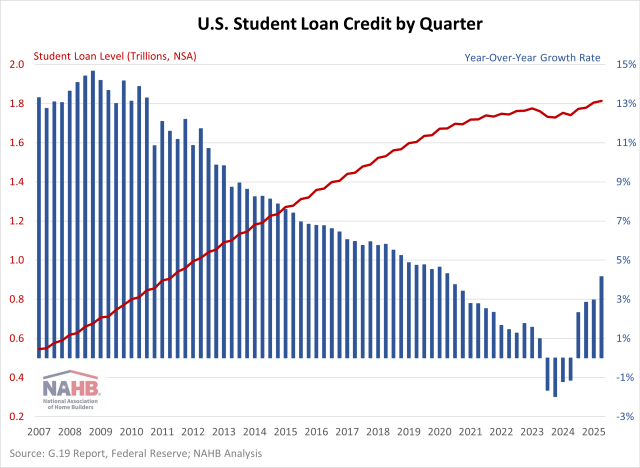

Student Loan Balances Rise

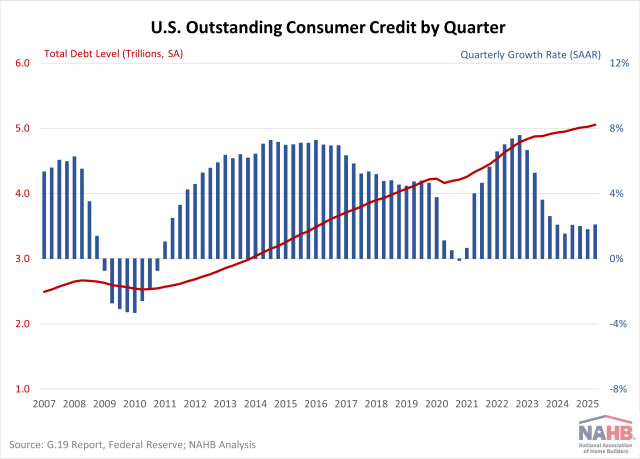

Overall consumer credit continued to rise in 2025, but the pace of growth remains slow. Student loan balances also rose year-over-year as borrowers resumed payments following the end of pandemic-era relief. Meanwhile, credit card and auto loan debt both experienced their slowest annual growth rates in years. Despite historically high interest rates, credit card and auto loan rates have eased slightly, providing some relief for consumers facing elevated borrowing costs.

Total outstanding U.S. consumer credit reached $5.05 trillion for the second quarter of 2025, according to the Federal Reserve’s G.19 Consumer Credit Report. This is an increase of 2.32% at a seasonally adjusted annual rate (SAAR) compared to the previous quarter, and a 2.09% increase compared to last year. Both rates have increased from last quarter.

Nonrevolving Credit

Nonrevolving credit, largely driven by student and auto loans (the G.19 report excludes mortgage loans), reached $3.76 trillion (SA) in the second quarter of 2025. This marks a 2.90% increase (SAAR) from the previous quarter, and a 1.94% increase from last year.

Student loan debt stood at $1.81 trillion (NSA) for the second quarter of 2025, marking a 4.16% increase from a year ago. The end of the COVID-19 Emergency Relief—which allowed 0% interest and halted payments until September 1, 2023—led year-over-year growth to decline for four consecutive quarters, from Q3 2023 through Q2 2024 as borrowers resumed payments and took on less new debt. The past four quarters have shown a return to growth, nearly matching pre-pandemic growth rates.

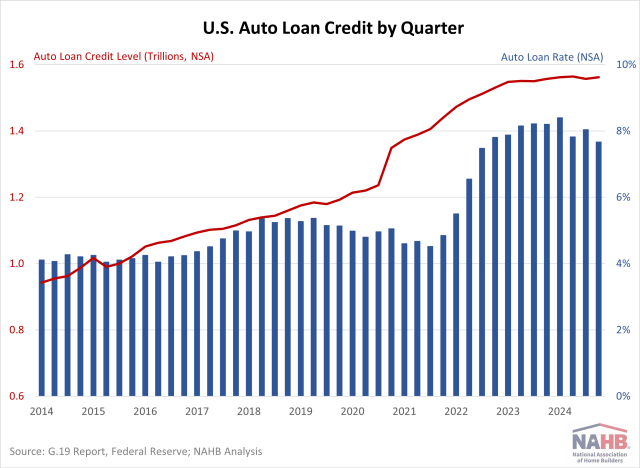

Auto loans reached a level of $1.56 trillion (NSA), showing a year-over-year increase of only 0.31%, marking the slowest growth rate since 2010. The deceleration in growth can be attributed to several factors, including stricter lending standards, elevated interest rates, and overall inflation. Auto loan rates for a 60-month new car stood at 7.67% (NSA) for the second quarter of 2025, a historically elevated level. However, auto rates have slowed modestly, decreasing by 0.53 percentage points compared to a year ago.

Revolving Credit

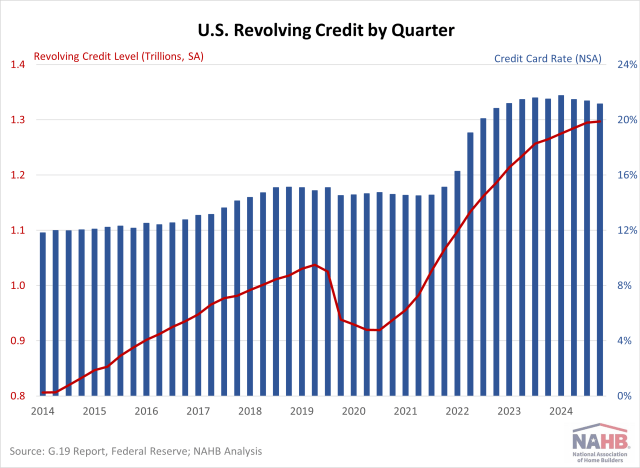

Revolving credit, primarily made up of credit card debt, rose to $1.30 trillion (SA) in the second quarter of 2025. This represents a 0.66% increase (SAAR) from the previous quarter and a 2.54% increase year-over-year. Both measures reflect a notable slowdown, marking the weakest growth in revolving credit in several years. This deceleration comes as credit card interest rates remain elevated, with the average rate held by commercial banks (NSA) at 21.16%. Although rates have hovered near historic highs since Q4 2022, the past two quarters have shown modest year-over-year declines, reflecting the impact of rate cuts that began in 2024.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.